|

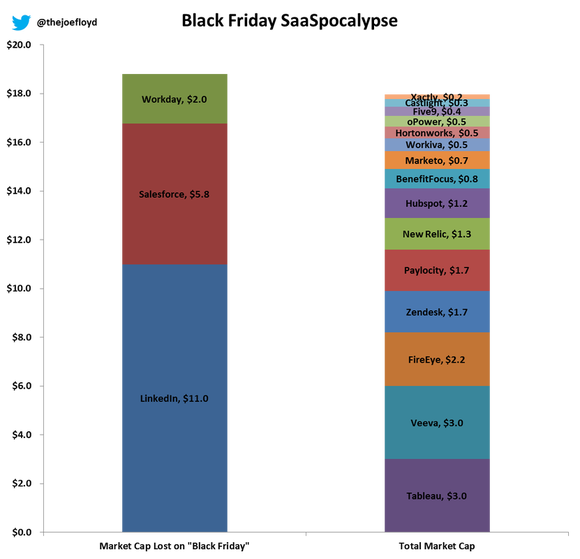

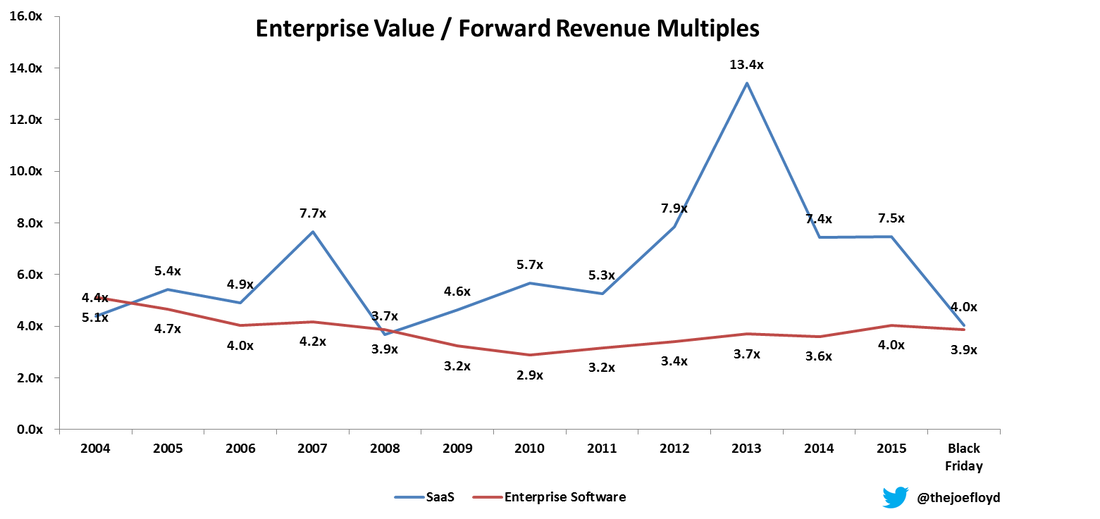

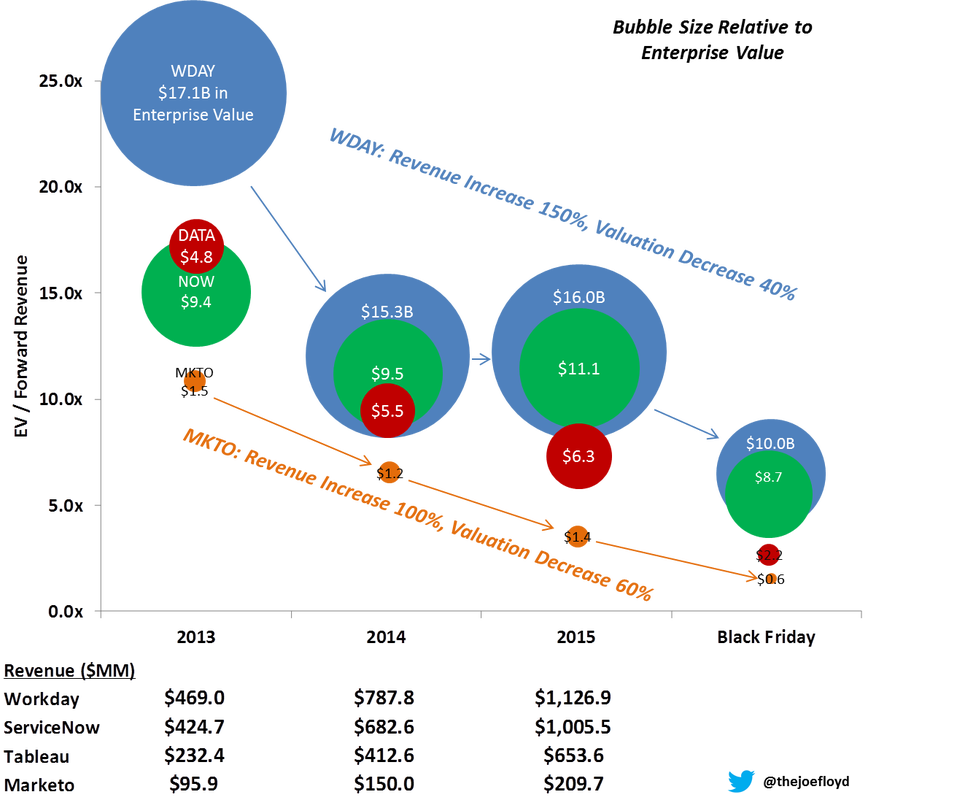

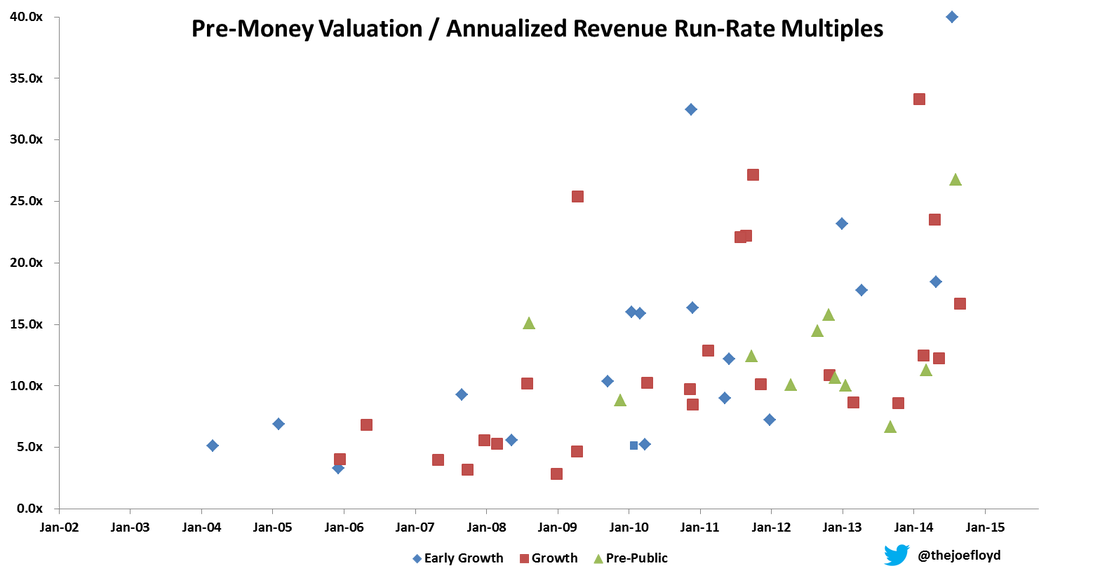

Last Friday, LinkedIn, Salesforce and Workday lost $18B in market capitalization. To put that in perspective, these three SaaS companies lost more in market cap on Friday than 15 current SaaS leaders are worth…combined.  How can this be possible? LinkedIn, Salesforce and Workday are growing revenue with sticky customers and they are targeting large addressable markets. Are they now suddenly undesirable companies? Investors Paid Yesterday for Today’s Growth On the contrary, public SaaS companies have largely met growth expectations and performed according to Wall St. expectations. The problem is that investors already paid for the projected revenue growth in many SaaS stocks a full 2 years earlier. Let’s look at historical multiples of Enterprise Value / Forward Revenue for the past decade. As you can see below, enterprise software multiples have largely held steady at 3-4x forward revenue. However, SaaS multiples began diverging in 2012 from their historical range of 5-6x forward revenue. This divergence peaked at the end of 2013 and has remained elevated above historical averages for 2 more years. The Black Friday correction brought SaaS multiples back in-line with enterprise software valuations. Like many corrections, the market has overshot to the downside as we at Emergence believe long term SaaS valuations of 5-6x forward revenue will return.  Note: Enterprise Software = Microsoft, Oracle and SAP. SaaS = Athenahealth, Castlight, Concur, Cornerstone, Dealertrak, FireEye, Marketo, Netsuite, Realpage, Salesforce, ServiceNow, Splunk, Tableau, Veeva and Workday. Growth Cannot Outrun Multiple Compression Recurring revenue business models are highly valued for recurring revenue and predictable growth engines. But what happens when predictable growth is no longer valued at predictable multiples? In the chart below, you can see what has happened to 4 of the hottest IPOs of the last few years. Workday has grown revenue from $470MM to over $1.1B in 2 years and yet their market value is down 40%. Marketo has doubled revenue over the last 2 years and their market value is down 60%. This is a really painful lesson for shareholders - it does not matter how fast revenue is growing if multiples are compressing faster.  There are number of factors that drive valuation multiples: future growth rates, operating margin and addressable market to name a few. For most of the public SaaS companies, the two main drivers of multiple compression have been decreasing revenue growth rates and diminishing risk appetite of investors. Lessons for SaaS Entrepreneurs So what does all of this mean for SaaS entrepreneurs? To be blunt, the issue of multiple compression is an even bigger challenge for valuations of private companies. Unlike the public markets which have regular earnings that ignite valuation changes, the private markets have very few catalysts for change. Private valuations have been driven upward by an abundance of capital pushing valuations higher and higher. You can see evidence of this trend in the scatterplot below of private SaaS valuations from the last decade.  Note: Early Growth = $2-5MM ARR. Growth = $5-20MM ARR. Pre-Public is $20MM+ ARR. I excluded certain outliers.

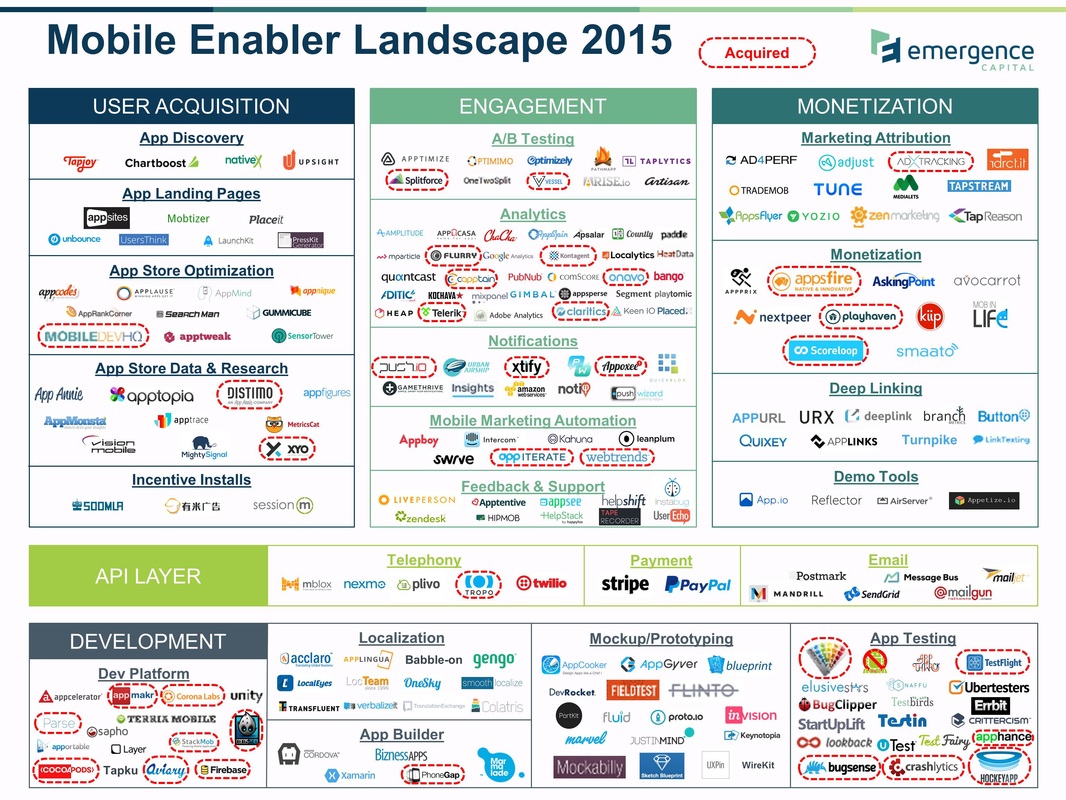

Similar to the public markets, SaaS valuation ranges began expanding in 2012. Unlike the public markets, private market valuations remained elevated through 2014. I purposefully truncated the data at the beginning of 2015 so as not to give away too much proprietary information. However, I will say that 2015 continued the trend until Q4 when fundraising became noticeably tighter – particularly in angel rounds and late stage rounds. The direct impact of a contraction in multiples is only felt when entrepreneurs are fundraising and the end result for the market is more flat/down rounds and more situations where a startup has to drastically cut burn. Here is a scenario that I’ve seen play out multiple times in the last 3 months. Hot SaaS startup raised a large Series A 12 months ago: $8-10MM at a $40MM post-money valuation. The company projected 2-300% growth on a base of $1MM ARR. Because they raised a large A, they accelerated hiring to hit aggressive growth targets and they are now burning $600K/month. Now, that same SaaS startup is at $4MM ARR and they want to raise $20MM and they expect a valuation of $100MM. Only now, multiples have compressed to 10x ARR. The entrepreneur does not like the dilution of $20MM in a flat round so there is a hard decision to make: raise less and drastically cut burn or raise what you need and suffer dilution. This situation can become a vicious cycle as sustaining growth is critical for future fundraising. This scenario oversimplifies the fundraising process and certainly every situation is different. However, the point I want to make is simple. The best entrepreneurs and best companies will be just fine fundraising even with a tightening market. It’s the startups with challenging cap tables, cost structures or market timing issues that will really struggle to fundraise. Black Friday isn’t the canary in the coal mine – it should be the last wake up call for SaaS entrepreneurs to take a good look at their business and make absolutely certain that they have a contingency plan for 18 months of cash. P.S. If you want to preserve cash without cutting costs, here are 5 cash flow hacks for SaaS startups. This post originally appeared in TechCrunch. Over the past three years, the Emergence Capital team has closely monitored the growing ecosystem of mobile enterprise applications. We have been fortunate to learn from our investments in a few of the early leaders across this landscape, including Box (collaboration), Doximity (digital health), ServiceMax (field service) and Cotap (enterprise mobile messaging). As we continue to watch the enterprise mobile app landscape develop, we have begun to formulate a thesis on the evolving ecosystem of SDKs (software development kits), APIs (application programming interface) and development platforms that mobile entrepreneurs are utilizing to accelerate the development, marketing and monetization of their mobile apps. Collectively, we are referring to these companies as the Mobile App Enablers, and we are starting to see some early trends. The landscape and industry trends we are sharing today are based on conversations with over 200 mobile app entrepreneurs and business leaders. We segmented the landscape of enabling technologies into three main layers:

Note that we specifically avoided categories like mobile ad networks or mobile device management.  Within the landscape’s three main segments, we have identified the following key insights:

Incumbent Web App Technologies Are Not the Leaders in the Mobile World Mobile app development is fundamentally different from web app development – from the programming languages to the hardware resources available to run an app and ultimately to the app store distribution model. As a result, web app technology incumbents do not have an advantage in most categories. For example, mobile specific development platforms such as Parse have emerged to solve very specific mobile app development pain points related to mobile devices and operating systems. We also found that the proliferation of mobile hardware created a new problem that could only be solved by mobile focused app testing startups like Crittercism. Lastly, with app stores serving as the gateway for user acquisition and monetization, we found that startups like AppAnnie (app store data) and ZenMarketing (attribution) started to solve very specific needs that their web counterparts like comScore and Convertro were not solving. The one major exception to this trend is that the API leaders which power the web also power mobile apps – Twilio for telephony, Stripe for payments and SendGrid for email. This makes perfect sense as developers are familiar with them and there is no real advantage for a mobile specific API technology in these general categories. There are a number of web incumbents who aggressively evolved their products to target mobile – Optimizely, Zendesk and Google Analytics are three examples. These companies should be lauded for their agility but they also face stiff competition from mobile specific startups and we will watch how their markets unfold. Mobile SDKs Need to Fight for Mindshare Due to app store approval processes, mobile app development cycles are slower than their web app counterparts. Also, the capabilities and storage of mobile devices are limited. As a result, mobile app developers are simply not willing to integrate an infinite number of SDKs. This has led mobile enabling technologies to fight for mindshare at the earliest stages of app development. Once a mobile app has integrated one analytics SDK, the bar for ripping it out and replacing it with a competitor is very high. We have observed the most successful SDKs like Mixpanel have targeted developers early with freemium offerings. Consequently, we have observed that getting your SDK distributed widely with freemium has enabled early leaders like Flurry to evolve their product offerings into other areas. Point Solutions Are Evolving into Suites Enabling technologies focused on driving engagement face stiff competition as illustrated by the highest density of logos on the landscape. As a result of this competition, we have seen this area evolve tremendously over the last six to twelve months. Companies like Leanplum and Swrve have moved from A/B testing to include customer segmentation and messaging. Mixpanel has evolved from analytics to include marketing automation features. Kahuna and Appboy have grown from just mobile marketing automation to email marketing and have displaced web incumbents like ExactTarget in accounts. This evolution is partially driven by market size and competition but also by the desire of customers to start paring down the number of vendors they integrate into their apps. The Fight on the Horizon As we look ahead, we know the number of mobile enterprise apps will continue to grow and this will benefit the ecosystem of enabling technologies. However, as enabling technologies mature, competition will increase – both from other startups and from the web incumbents who rapidly attempt to catch up. We anticipate consolidation within the major categories on our landscape, particularly as the early leaders broaden their capabilities into product suites. We realize that we have likely missed some great companies, so please let us know if we missed you. Also, if you are thinking about other frameworks to categorize mobile enabling technologies, we would welcome sharing ideas. In October, I published this article in TechCrunch on how to tell if your SaaS startup was burning money too fast. That blog post spawned a number of great conversations with entrepreneurs on how to measure and control cash burn. The ugly truth is that startup CEOs have to walk a fine line with cash burn: spend too little and your startup may not grow fast enough to achieve escape velocity; spend too much and your startup might run out of life.

“Why don’t I just spend money to experiment and then dial back when it isn’t efficient?” – This line of thinking is perfectly logical but the simple truth is that it just isn’t very easy to cut costs without hurting employee morale, disrupting culture and killing your revenue momentum. However, given the SaaS business model, you can apply a little financial hacking to conserve cash without cutting spend. Here are my top 5 SaaS financial hacks: 1. Focus on annual contracts and collect the cash up front. Sales reps are naturally inclined to go for the monthly sale – it seems easier because it is a smaller commitment. That’s true, but it kills your cash flow in a couple ways: one, monthly contracts churn at a higher rate than annual; and two, monthly contracts require a long time to pay back the initial sales and marketing cost to acquire that customer. For example, let’s say your gross profit pays back customer acquisition cost in 9 months. That means you are cash flow negative on that customer for the first 9 months and you will take a permanent loss if that customer churns in that time period. Now, let’s assume you only sign annual contracts with payment up front. That same customer is immediately cash flow positive and you can never take a permanent loss because their first opportunity to churn is at the 12 month mark. It sounds simple because it is. Incentivize your sales team to sell annual contracts and incentivize your customers through small discounts to pay upfront. 2. Implement faster and thus invoice faster and upsell faster. “Awesome, my sales team just sold an annual contract, but where is the cash?” For most enterprise customers, you do not invoice your customer until your application is implemented and live. For customers that require integrations, training and set up time, this presents a significant delay. Improve your cash flow by compressing the time from signed contract to live deployment. Plus, you’ll get an added bonus – the faster a new customer goes live, the faster your customer success team can upsell additional features and more seats. 3. Match sales commissions to cash flow. “Wait a second! While I’m waiting for implementation to finish, I’ve already paid out the sales commission so my cash flow is even more negative.” That’s right! That’s why forward thinking sales leaders find ways to match the timing of sales commissions to the cash flows of new contracts. There are many different ways to do this without causing too much disruption. The key is to make sure reps see the new system as fair and transparent. 4. Extend accounts payable and speed up collections of accounts receivable. I am constantly amazed by how quickly startups pay their bills. It’s time to start thinking like a big company – maximize your float and set up your bills to be automatically paid close to their due date. More importantly, don’t let your customers borrow from you interest free for 90 days. Test the best way to improve the speed with which your customers pay you – you can discount for early payment, you can send invoices early and you can even just try using personal charm on the accountants. If a company with $6MM in revenue can bring its accounts receivable days outstanding from 90 days to 60 days, the net gain is $500K in cash. 5. Shift capital expenses to operating expenses. Capital expenses for startups are items like office leases, furniture and computer equipment. For example, office leases may require hefty deposits or payment upfront and furniture is often purchased in advance of new hires. You can save cash by shifting these fixed expenses into monthly rentals. SaaS startups already face an uphill battle given the business model of initial customer acquisition costs which are paid back over time by subscription revenue. Using these 5 SaaS financial hacks can conserve cash and extend your runway without reducing spend in your product or sales organizations. Questions about cash burn have blazed through Twitter like wildfire. Entrepreneurs are asking us: How do I know if I am burning money too fast? Unfortunately, there is no one-size-fits-all answer for an entrepreneur on what level of burn is appropriate for their startup. However, every entrepreneur should consistently assess their runway and revise spending against their strategic goals.

I have designed this short quiz to help enterprise cloud startups analyze their spending levels. It’s critical to monitor your company’s burn rate so you can make those quick adjustments to increase your chances of success. Select the answers below that best describe your company. 1. Market Dynamics: Does your market have network effects? a) Each sale is independent. If we sell to one customer it does not impact the likelihood of sale to another customer. b) Economies of scale are important in our market and we believe that only three or four solutions will achieve scale. Early movers have a small advantage. c) Every new customer increases the value of our product and becomes a source of new potential customers. Early movers have a major advantage. 2. Competitive Intensity: Who are your major competitors? a) We are in a dogfight with a number of well-funded startups and large incumbents. Our sales team consistently sees competition for new customers, and we win as often as we lose. b) We are competing with one or two large, entrenched companies. Our sales organization sees competition more often than not, but we win most of the time. c) We are carving up a green-field opportunity. We sometimes face competition for new business but it is usually from consultants or internal teams building custom solutions. 3. Customer Retention: What is our churn? a) We estimate that we turnover 1 out of every 4 customers each year. We haven’t really started tracking churn yet, but I would guess that our net annual MRR churn is ~20 percent. b) We track churn and we know we retain 85-90 percent of our customers annually. We have increased our average sales price by 10 percent over last year. We also have a customer success team that upsells our most engaged customers, so our net annual MRR churn is only 10 percent. c) We track each cohort of customers on a monthly basis and our customer success team excels at deploying new customers quickly and getting them engaged. We have negative MRR churn, and each monthly cohort continues to grow over time. 4. Sales and Marketing Efficiency: What is the return on every dollar of sales and marketing spend? a) We spend $1 – $1.5 in sales and marketing for every dollar of total bookings (new and renewal). We do not worry about gross margins because we know they will increase with scale. We collect some contracts monthly, quarterly and annually. b) We achieve a 1:1 ratio of sales and marketing spend to new annual contract value (ACV) bookings. We analyze customer acquisition costs (CAC) by channel, and we tend to payback CAC with gross profit in 9 – 12 months. We try to get cash payment up front for annual contracts. c) We consistently receive $2+ dollars of new ACV bookings for every dollar of sales and marketing spend. We optimize CAC by allocating marginal spend to the highest performing channels. Gross profit pays back CAC in less than 6 months consistently. Our customer success team is deploying signed contracts quickly, and we always collect cash up front for our contracts. 5. Fundraising Capability: Who is in your investor syndicate and how easily can you add new sources of capital if you need to fundraise quickly? a) We have a group of angel investors or constrained institutional investors. It feels too early to pursue debt. We are heads down focused on sales and product right now and we will think about the next fundraising when we need to raise more money. b) We have one institutional lead investor with dry powder, and we think we can secure a small debt facility. Our investor can introduce us to venture firms so we can start a fundraising process pretty quickly if we need to do that. c) We have two or more institutional venture investors and we have a small debt facility with our bank that we can draw down if we need it. We keep a steady dialog going with investors that we would like to involve in future financings so we could start a process tomorrow if desired. What’s your score? Give yourself one point for each “A” answer, three points for each “B” answer, and five points for each “C” answer. 0-10 points: Pull the ripcord. You need to evaluate your spending immediately and consider pulling back drastically. You may be too early in a nascent market, and it would be wise to conserve capital until the market develops. You may be facing too many competitors which is forcing everyone to spend inefficiently. You may want to scale back sales and marketing while you pivot your product to find a more attractive competitive position. Lastly, you may not be able to raise additional equity if the current venture environment sours. You should look to secure a debt facility and reduce burn to give your team the longest possible runway to succeed. 11-18 points: Pump the brakes. You are not in trouble yet, but you should quickly assess your situation. If you are targeting a large enough market, then you may be justified in continuing to spend on sales and marketing even if you are not that capital efficient. However, you should drill down and figure out why you are not efficient. Do you have a churn problem? Do you face too much competition? Do you have too many sales reps? Not enough good sales reps? Are you marketing in the right channels? Is your pricing right? Is your product truly solving a customer pain point? Once you understand the drivers of your current business, you can reduce spend in the areas that are not efficient. For example, if you do not quite have product-market fit, then you can reduce sales. If you do not have sales functioning perfectly, you can reduce marketing spend. Lastly, you should consider raising a top up round to give yourself 18 months of runway while the venture fundraising window is open or securing a debt facility to give yourself an extra 6-9 months of cushion. 19-25 points: Burn baby burn. Your sales and marketing engine is firing on all cylinders and you have proven you know how to engage customers and keep them renewing. Now is the time to pour fuel on the fire to attack your market while there is little competition. The viral effects are strong enough to justify the investment now, and investors will reward you for your efficient growth. Remember to keep monitoring your SaaS metrics so you can adjust your spend if your business slows down. Lastly, you should consider raising additional growth equity early while the venture window is wide open and valuations are aggressive. Editor’s Note: Joe Floyd is a venture investor at Emergence Capital. Emergence focuses on enterprise cloud applications and has invested in market leaders including Yammer, Box, Veeva Systems and Salesforce. This post originally appeared in TechCrunch. Talented engineers are the lifeblood of software startups. Unfortunately for Silicon Valley, talented engineers are in short supply and the competition for their services is as fierce as ever. Given this market dynamic, many of our portfolio companies have made the decision to open engineering offices outside of the US. While initially skeptical, I have come to appreciate the competitive advantage of having access to the global talent pool. In order to help other startups that are thinking of hiring globally, I sat down with a handful of CEOs to learn more about their experiences. Below is a summary of benefits and best practices.

Benefits

Best Practices Selecting a Location - So where do you set up shop? As any good real estate agent can tell you, location is everything. Every CEO gave the exact same advice: choose a location where you already know someone that you absolutely trust. You can find talented engineers almost anywhere, but it is critical to have the first person on the ground be someone you trust and someone that can recruit the best talent in that location. Here are the top three location specific advantages cited by CEOs:

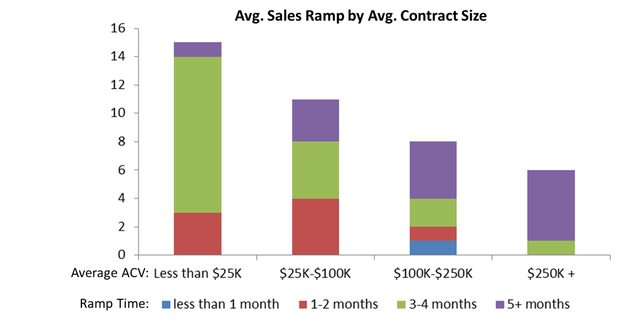

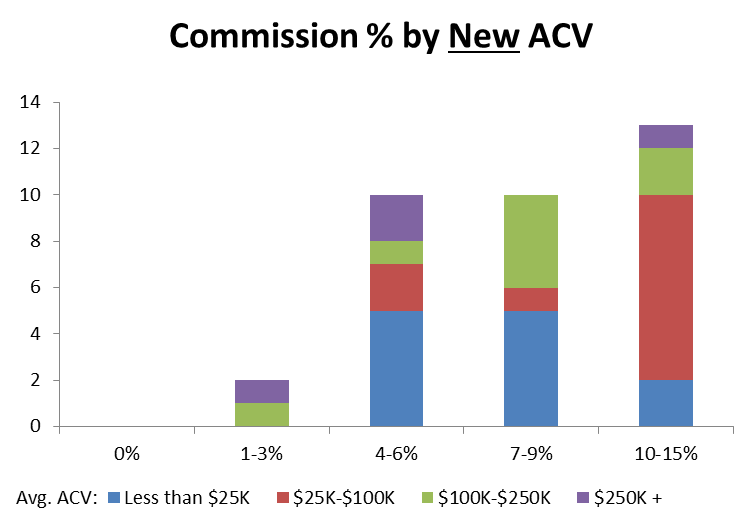

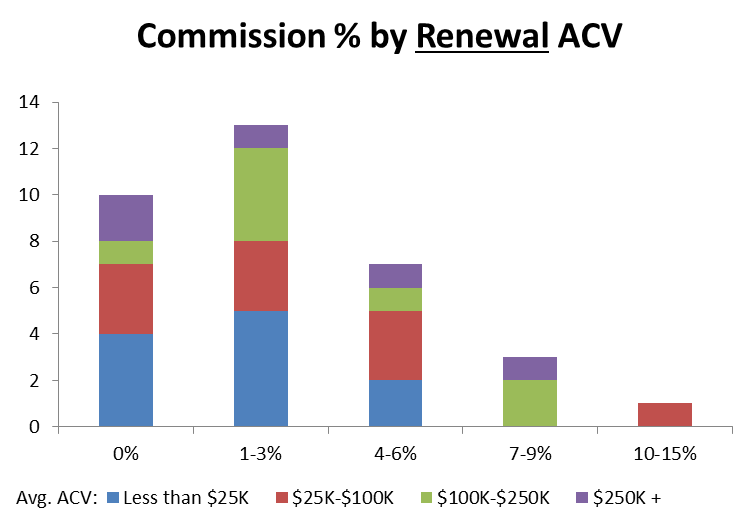

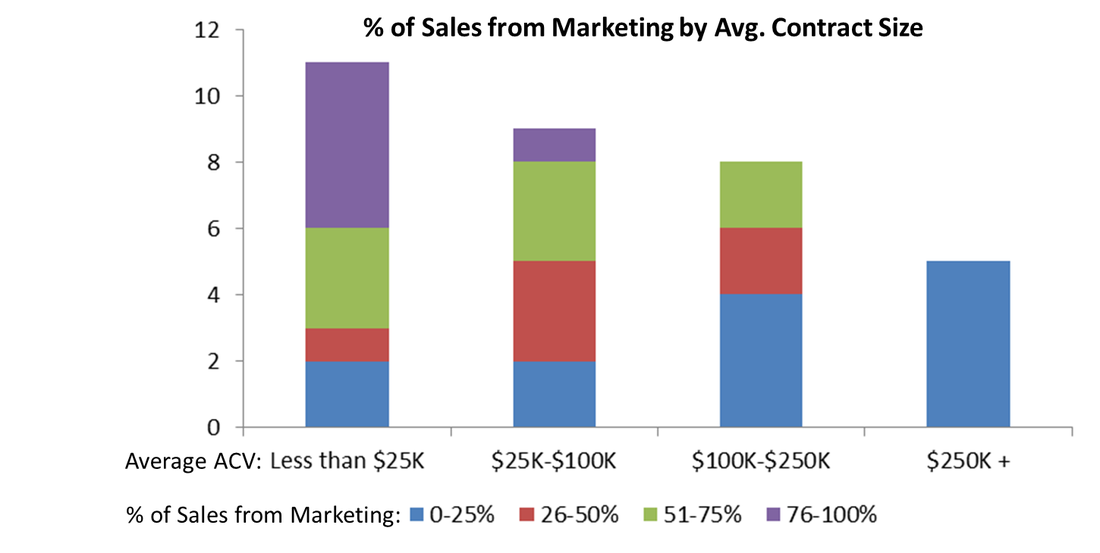

Closing the Distance - After hiring people you trust, the next most critical factor in determining your success with remote technical talent is how you implement work flows and processes to integrate your organization. CEOs point to a number of collaboration tools including Zoom, Yammer, Skype, Hall and Hipchat. One popular setup uses Slack as the platform which ties into a variety of systems like JIRA for project management, Github for code, Heroku for deployment and Zendesk for customer service. Slack can be set up to receive automated notifications from these development tools. Using Slack as the central information repository is a slick way to keep everyone informed and up to date across geographies and time zones. Every successful startup has at least one unfair competitive advantage and leveraging the global nature of technical talent provides a few: scale faster than the competition, retain your talent and reap the benefits of global locations. With today’s modern collaboration tools, global talent is more accessible than ever and our startups are taking advantage. Emergence’s singular focus on enterprise applications gives us unique insights across the landscape of enterprise cloud companies and we love sharing those insights with our executive teams. We recently gathered our portfolio sales and business development leaders for our annual revenue summit. As part of the summit, we gathered data across the attendees and we wanted to share the top 10 insights.  Insight #1: Companies that sell larger average contracts tend to have slower sales productivity ramps. When sales leaders begin hiring reps for larger contracts, they need to plan for that ramp time in their forecasts.  Insight #2: Commissions for new ACV vary widely by size of deal. In our experience, there is more of a direct relationship to the overall quotas for reps and the commission percentages.  Insight #3: Most sales leaders offer lower commissions on renewal ACV and nearly 1/3 offered no quota on renewals. We find that most of our revenue leaders have bifurcate quotas for new business to sales and renewals to customer success.  Insight #4: Marketing drives the majority of sales for smaller ACV deals. This can be interpreted in two ways: one, companies with smaller average contracts need to invest more heavily in marketing to be efficient; and two, every company needs better attribution to figure out the impact marketing dollars are having on end customer sell through. Insight #5: 70% of sales leaders surveyed hired 50% or more of their reps using in-house resources. Scaling sales reps is not easy, particularly in the growth stages. The best companies build in-house recruiting organizations and tap their employees for referrals. Bonus Insight: Here are the most commonly used sales enablement tools among our revenue leaders. Thank you to all of our portfolio executives and guests for sharing your knowledge and energy at the 2014 Emergence Revenue Summit. See you next year!  Lured by the success of companies such as Workday and Marketo, consumer internet and mobile entrepreneurs have flooded into enterprise startups.

This new wave of entrepreneurs has leveraged their consumer DNA to reimagine the way enterprise users consume software. They have injected beautiful design and streamlined user experiences, which make their software seem both fresh and familiar to users in a business setting. However, the best product does not always triumph in the land of long sales cycles, custom integrations, and the dreaded procurement officer. In order to win in enterprise markets, startups need to build world-class marketing, sales and services organizations. Today’s product-centric entrepreneurs should follow in the footsteps of market leaders such as Box, Yammer and Veeva Systems and reevaluate these three common startup myths from the consumer internet: Myth #1: If our product is great, then word of mouth virality and organic search will generate the web traffic necessary to drive growth. Organic search and word of mouth virality are great for acquiring individual users, but they are not sufficient for grabbing enterprise decision makers. For example, Box has a freemium product with virality built-in through file sharing. This customer acquisition channel can generate enough paid conversions to sustain meaningful growth at the consumer and small to medium business levels. However, when it comes to generating enterprise leads, demand generation techniques are absolutely necessary to feed an enterprise sales team. Box uses a combination of content/influencer marketing, paid search/display advertising, conferences and channel partners to target and build a pipeline of decision makers. Myth #2: If our product is easy to try and customers can sign up with a credit card, then I do not need expensive sales reps to sell it. Self-service sales models work very well in situations with single decision makers and low price points. However, self-service models break down at the enterprise level. Yammer built a great self-service model where SMBs or managers within an enterprise could sign up a team with a credit card. Yet when it came to enterprise-wide sales, Yammer discovered that inside and direct sales reps were necessary to manage and win enterprise contracts. In particular, sales reps are able to sell to multiple decision makers within an organization, push contracts through procurement, compete in RFPs and negotiate service level agreements and integrations. Myth #3: If our product is designed so that it is intuitive and easy to use, then I will not need professional services. Low or no-touch service models are critical for consumer startups given the scale of their customer base. However, customer success and professional services organizations are critical for success with enterprise customers. Veeva Systems has built a world-class services organization that provides three key strategic advantages:

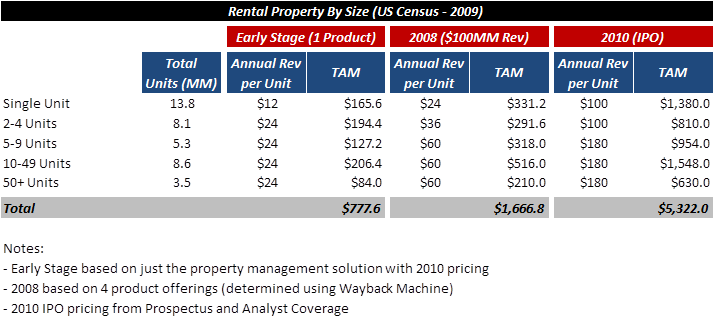

When consumer startups scale, they require capital to expand the product and support the user base. Conversely, when enterprise startups grow, they require capital to scale sales, marketing and services. When an enterprise startup is seeking a Series A investment, veteran investors will not expect that the CEO has definitively cracked the code on scalable demand generation, predictable sales and customer success. However, we absolutely want to see that startups have experimented to test hypotheses in each of these categories. Designing experiments, tracking metrics and iterating quickly are critical proof points that allow entrepreneurs to earn trust with investors because it demonstrates that they will spend capital efficiently. Consumerization of IT has led to a renaissance of enterprise software. Now that entrepreneurs are designing delightful enterprise products, they cannot ignore the need to build the sales, marketing and services engines necessary to deploy that software into the hands of enterprise users. As more enterprise solutions are coming to market, VCs will be even more discerning as they decide where to invest, so it is important for entrepreneurs to not fall prey to the myths of the consumer internet. This post originally appeared on Entrepreneur. According to a Sarah Lacy article from earlier this year, Andreessen Horowitz almost had an iron clad rule to never invest in verticals. The main reason to avoid vertical investments was because they had small addressable markets and thus it was difficult to build a big business. Thankfully, Emergence ignored traditional thinking and bet early on Veeva Systems (NYSE: VEEV). What did we see that made us think it was a big enough market? We had a core thesis that SaaS made verticals more attractive. SaaS products can evolve faster than on-prem deployments and thus, we believed vertical SaaS applications could achieve high levels of customer satisfaction by combining vertical market expertise with rapid, focused iteration. This customer satisfaction would enable vertical SaaS vendors to perfect a use case and then sell additional products and services to their happy customer base. Let’s look at RealPage (NYSE: RP) as an example. RealPage sells web-based property management solutions to the multifamily real estate industry. Using the 2009 US Census, I used a bottoms-up approach to calculate total available market size for RealPage with their initial product at ~$780MM. By 2008, RealPage had expanded its product offering and increased ASPs almost doubling their market size to ~$1.7B. Lastly, at the IPO, analysts projected future growth in product offerings which tripled market size to ~$5B.  Away from the fickle eyes of consumers, deep in the basement of app stores, enterprise mobile apps are fighting each other for the attention of business users. Given the restrictions of their target audience, business app developers simply cannot utilize the same techniques that consumer app companies leverage. Why is that? And more importantly, how can mobile business apps efficiently speed up user acquisition?

Customer Acquisition Models For Consumer Apps First, let’s examine the methods consumer app developers have used to efficiently acquire large user bases and why business app developers cannot leverage the same techniques. Obviously, consumer apps have a large target audience as everyone with a smartphone is a potential customer for a consumer app. As a result, the size of the target audience is capable of generating enough web and app-store search volume to build an initial customer base for apps. Plus, the undifferentiated nature of consumers means that cross promotional advertising on consumer apps can be a very effective and efficient user acquisition technique. For example, an advertisement for a mobile game can appear on any mobile app and the end user is always a potential target. On the contrary, the target audiences for business apps are often much smaller and may be focused on a particular vertical niche such as doctors or real estate professionals. As a result of the smaller target audience, business apps do not see a sufficient level of web and app-store search volume. Further, cross promotional advertising is much less effective because of the niche target audiences. For example, less than 1% of US smart phone users are doctors, which makes it very difficult to target that vertical with display ads. Lastly, consumer app developers with deep pockets have been known to game app store rankings. At the launch of a new consumer app, the developer can pay for downloads through services, such as Chartboost and Tapjoy, until they crack the top 25 of an app store. At that point, their visibility on the app store leaderboard increases their discoverability to the point where organic downloads can take over. Given their smaller target market, mobile-first business apps simply cannot compete with consumer apps for space in app-store rankings (there are no business apps in the iOS Top 50 as of this writing). Building Virality Into Enterprise Apps Now that we’ve explored what is not working for enterprise mobile apps, let’s focus on what is working: designing your product work flows to drive direct exposure to new potential users and building in opportunities for indirect referrals through word-of-mouth virality. Dropbox is the quintessential paradigm of designing virality into a product. Users are incentivized to refer Dropbox because they receive free additional storage for doing so. Additionally, the act of sharing a file with a friend inherently exposes Dropbox to new potential users and serves as a trigger for customers to talk about the service. Building on the lessons learned from Dropbox, there are three techniques that emerging mobile-first business app developers are using to build virality into their products: triggers, incentives and work flow. Triggers are events that spur an action. In this particular context, triggers are actions that an app user takes which provide for an opportunity to discuss the application. Expensify, a mobile app for business users to submit expense reports, has built in two word-of-mouth referral triggers: 1) every time a user takes a picture of a receipt for expense reporting, they are triggered to talk about the app with the coworkers or clients present; 2) the act of submitting an expense report triggers an explanation of the product to the person approving the report. Incentives play on the concept that users are much more likely to actively refer a product if they receive some practical value for doing so. Plangrid, an iPad app for managing construction-site blueprints, uses incentives to spread among the different companies that collaborate on construction sites. Plangrid’s value to each site user increases with each additional company and user that joins and adds to the project. Thus, users have a practical incentive to refer the product to new target users. Lastly, building virality directly into the workflow of how a customer uses an app is a very effective way to expose the app to new potential users. Doximity, a mobile professional network for physicians, has built virality into its product workflow through its secure messaging capability. Doctors use Doximity to send HIPAA compliant messages to other doctors. Every message sent from a user to a doctor not yet on the platform exposes a new potential user to the product as the message recipient must install Doximity to read the message. Key For Enterprise Apps Mobile-first business apps have to follow different rules for customer acquisition in order to achieve the scale and marketing efficiency of their consumer-focused brethren. The key for enterprise apps is to focus on building virality into the product so users directly or indirectly spread the app within their target audience. The mobile-first business apps that emerge victorious will be the ones that leverage triggers, incentives and work flow to kick their user acquisition flywheel into overdrive. This piece originally appeared in TechCrunch. This piece originally appeared in VentureBeat.

Consumer-to-consumer (“C2C”) marketplace startups are enjoying a Renaissance, as exemplified by Airbnb and others. Sites like these that facilitate transactions between people have disrupted older offline business-to-business marketplaces by taking advantage of ubiquitous mobile access, and delivering a better experience. This recent C2C marketplace success is spurring a new crop of similar business-focused ventures, which I believe have tremendous potential to leverage the unique synergies of combining the marketplace model with the software as a service (“SaaS”) platform. By serving as the access portal to the marketplace, the system of record and most importantly, the paywall that drives predictable revenue, SaaS can revolutionize the marketplace model to offer modern advantages the failed B2B marketplaces of the early 2000s never had. These include revenue predictability, favorable unit economics and a barrier to disintermediation. Here are the three key advantages of SaaS: Larger market size and revenue predictability In the late 1990s, Zoho Corp. emerged as an online marketplace for hotel supplies that raised $63 million. Targeting the massive hotel industry ($120 billion in revenue in 2012 according to IBIS), Zoho operated on a transaction model whereby the company received a small percentage of each transaction. This transaction model severely limited revenue potential and made commissions unpredictable. Zoho ultimately shut down when key buyers, including investors such as Harrah’, purchased only a small fraction of products from the heavily commoditized hotel supply chain. As a result, Zoho earned small commissions on low margin business with little predictability. Today, business marketplaces can use SaaS platforms to increase market size and improve revenue predictability by selling subscriptions to access and manage the marketplace. For example, LiquidSpace enables individuals to reserve meeting rooms, conference or office space at commercial venues such as hotels. As a transaction marketplace alone, the market size is similar to Zoho’s which aimed to apply a small commission to a large target market and win by capturing volume. However, in addition to monetizing transactions, LiquidSpace also sells their platform directly to hotels (50,000+ potential), universities (100,000+ potential) and enterprises (potentially in the millions) as a service to manage their own meeting spaces internally. These internal networks greatly increase the market size opportunity as well as revenue predictability with a monthly subscription service instead of a transactional model. Further, adding subscription customers with internal networks of captive guests, students, and employees greatly increases the number of individuals with access to the public marketplace since it is all one platform. Better Unit Economics Every successful startup faces competition and, eventually, margin pressure. This is particularly true for transactional marketplaces. For example, oDesk, Elance and 99Designs are all sizable marketplaces that connect jobs with freelance workers. But, the success of these marketplaces drove up the cost of keywords used to acquire traffic and drove down the price of jobs (and therefore net margin to the marketplace provider). On the other hand, using a SaaS-based subscription model, business marketplaces can improve unit economics in three ways:

For example, Scripted connects businesses to freelance journalists through its online marketplace. Since Scripted sells access as a SaaS subscription, businesses sign annual contracts (which lowers churn) with Scripted supplying a minimum quantity of written content. If the customer does not utilize the full quantity of service, subscription breakage occurs – Scripted still earns the full revenue but does not incur the cost of providing the unused service (which expands margins). In combination, these two forces increase customer lifetime value, allowing Scripted to increase sales and marketing spend to scale growth more aggressively. A Barrier to Disintermediation The threat of disintermediation should be top of mind for any good middleman. Marketplaces serve as insurance to both supply and demand and provide the necessary security to complete transactions in an uncertain environment. However, once a network connects two parties, nothing prevents them from circumventing the platform and dealing directly. For example, MetalSite, one of a few vertical specific marketplaces in the early 2000s, connected commodities buyers and sellers via auctions. But, MetalSite and many other vertical B2B marketplaces failed because they were taken out of the loop after the first transaction as suppliers began bidding lower prices directly to buyers, without paying commissions to MetalSite. On the other hand, OpenTable, a restaurant reservation marketplace, has become the de facto system of record for many customers. As a result, customers are locked in to using the platform, which ensures OpenTable captures each transaction and receives its commission. Additionally, restaurants are much less likely to replace OpenTable with a competitor because it keeps the system of record as opposed to simply being a source of reservations. Final Thoughts The initial wave of business-focused marketplaces crashed in the dotcom bust because they focused on transactional pricing, competed with incumbents on price and failed to build relationships with their marketplace participants. We are in the early innings of a new wave of business-focused marketplaces that are likely to succeed, thanks to SaaS, which can serve as the system of record, and generate predictable revenue. People often ask me, "How can I get a job in venture capital?" There are a plethora of different paths to landing a gig in VC, but there are really only four well-traveled roads:

I was incredibly lucky to have navigated path #4 and doubly blessed that I landed with the amazing team at Emergence Capital. Here is the four step method I used to improve my chances:

I developed 4 different Investment Idea Presentations and I tailored the companies in each presentation for the person I pitched. I probably had a 50/50 ratio of getting a meeting and I ultimately talked to at least 30 different investors. Out of those 30+ individuals, I came across only 4 firms interested in hiring an investment professional and I was fortunate enough to land with my top pick. Han Solo said, "Never tell me the odds." Well, I just told you the odds and hopefully gave you the edge to overcome them. Good luck! |